Is An Index Fund Really A Universal Fix?

Billions of dollars are invested in index funds but not all funds are created equal

“It’s great for now, I just don’t know when it’s going to stop,” I said, talking to a friend about the current stock market. We were discussing recent podcasts featuring Ray Dalio and what he has said about the economic storm to come, and talked a little about Dalio’s all-weather portfolio. Both of us are aware that the golden days of the U.S. stock market may (or may not) have come and gone.

For the last few decades, just throwing your money in an index fund has been a damn good strategy. But any investor of any length of time in the market is aware that something is coming. I think of us old investors as old sailors who can sense the coming weather. A recent post from the excellent Substack The Purse backed up some of what I’m thinking about lately, that maybe index funds won’t be as valuable a tool in the future or at least that index funds need careful watching.

Of course, the first question is which index fund. Generally, when people say "index fund," they mean the S&P 500, which, in theory, represents the 500 companies with the best prospects for continued growth and stability. However, anyone who follows the market is aware that seven of the 500 stocks have been doing the heavy lifting lately, and most of that growth is tied to artificial intelligence. History tells us that every new technology brings a boom and, if not a bust, at least a modest crash. Great things come out of those crashes, but they are painful to live through, and one never knows how long the recovery will take. Index funds that hold only the S&P 500 and are weighted toward market cap or another metric rather than holding all 500 equally are delivering more growth right now, but also carry higher risk.

As I ponder all of this, I’m reading an investing classic: “A Random Walk Down Wall Street” by Burton Malkiel. This is the book that spawned dozens of other investing books and has sold over two million copies. At one point, every investor hears of it; it should be in any core curriculum. Malkiel carefully goes through all types of investing techniques, breaking down the mechanics behind the chartists (the people staring at market fluctuations and discerning patterns); the fundamentalists poring over earnings reports; the quants measuring beta; the behavioralists applying psychological techniques to market trends, and everyone else trying to figure out what may happen next.

What every investor is after is the illusion of control. Your money, whether it is your nest egg or money you manage for someone else, is just out there, a boat in the ocean at the whims of the tides. Given that, does the broadest portfolio make sense? It depends on what you consider broad. Owning every stock out there makes no sense (so many clunkers); you wouldn’t own enough of the good stuff to make the bad stuff worth it. And there’s no guarantee that stock owning is the best strategy.

One great thing about the proliferation of ETFs is that you don’t have to put your portfolio into one strategy. Diversification can be more than owning just one index fund or even one version of an index fund. This may involve incorporating a range of strategies. The friend mentioned above and I also discussed the merits of QQQI versus JEPI, both covered call ETFs with different takes on delivering income. If you don’t have a friend who likes to talk about investing, I highly recommend finding at least one, you at least have one in me.

You can drive yourself nuts with comparisons of the thousands of ETFs out there, but choosing a couple of different paths rather than a single strategy feels like a good option. Like me, Malkiel likes REITs, which have been creamed in our recent growthy markets but may still deliver over time (Vanguard’s VNQ is a good option if you don’t want to buy individual REITs). Time is the friend and the enemy of the investor: have enough of it and you can make a lot of mistakes, have too little of it and you can’t take the big risks that can but often don’t yield rewards.

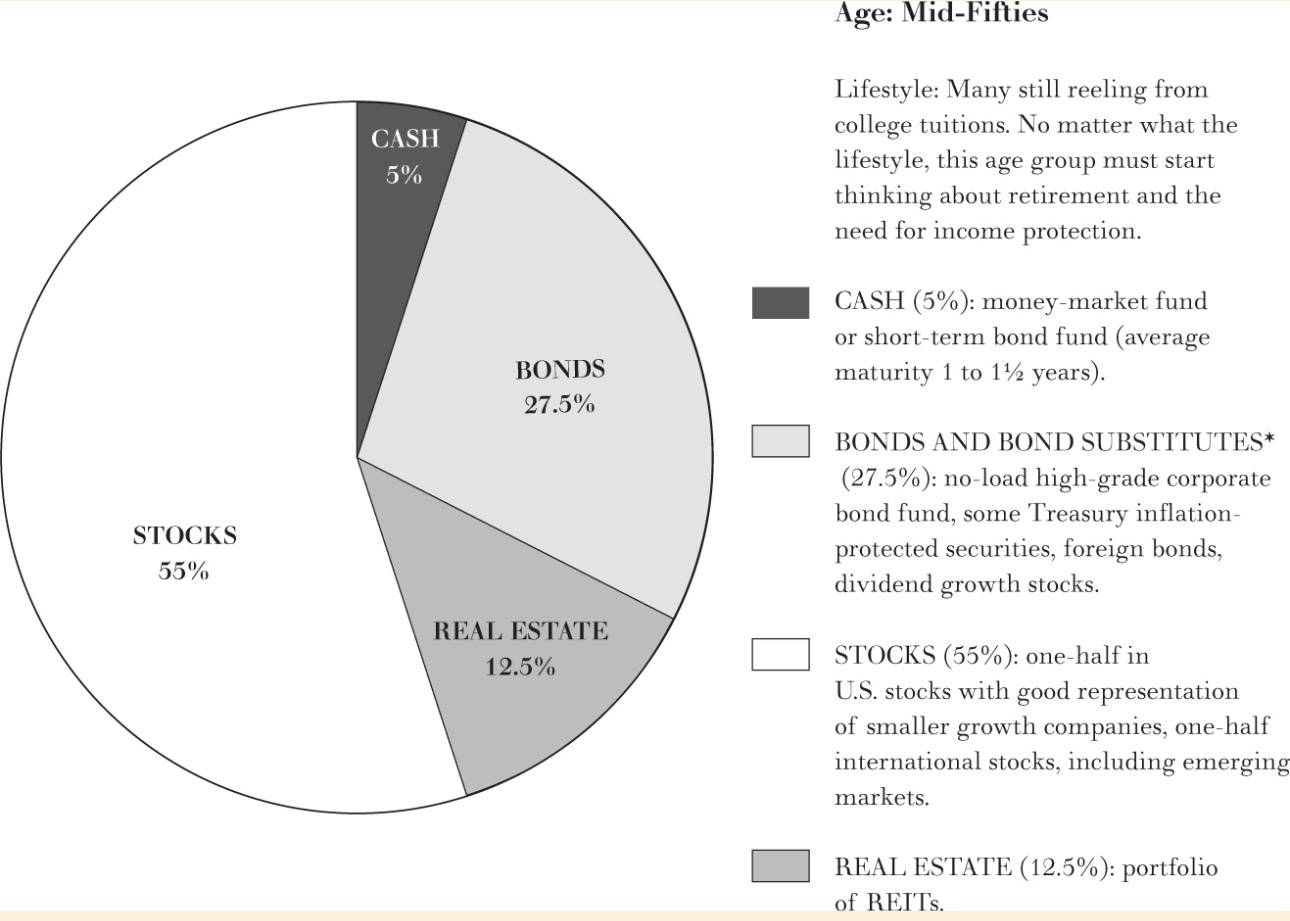

Malkiel takes this on with different portfolio allocations by age. I’m sharing the mid-fifties one below since that’s where I find myself. He takes the old rule of your age correlating to how much of your portfolio should be in stocks and tweaks it slightly by adding bond alternatives, including dividend-paying stocks, bonds, and REITs in real estate. I think this is a pretty decent place to start, and I like that he specifies international and small-caps as part of a stock portfolio. My personal portfolio isn’t quite here yet (not enough bonds and not enough international, but close

It’s not just Wall Street that is a random walk; it is really all of investing that is part luck, part riding the bull while it tries to throw you off. A couple of years ago, I interviewed Greg Harden, famous for being Tom Brady’s college coach and author of a book titled Stay Sane In An Insane World, and the thing I learned from him is to control the controllables. Don’t bother worrying about things you have no influence over. Your area of control in investing is where you put your money, how much it costs you to do so, and how much you pay taxes on it.

Malkiel first wrote this book in the 1970s; it has been revised multiple times as rules and tools have changed, but the philosophy remains the same: develop a solid plan for saving and deploying cash, build a balanced portfolio with a wide variety of investments, keep an eye on your taxes, and adjust as needed. You can spend as much time or as little tinkering around, but the results may end up being mostly the same. I have my theories about what may be next for the economy, but I believe over time, the strategy in this book is as solid as it was decades ago.

The linked essay below is a fascinating exploration of the effect of widespread indexing on market structure and price action. It would be quite interesting to know your thoughts about it, if/when you’re inclined…

https://www.acheroninsights.com/blog/wbdvi4uarbd3hdssx3f5kaffkz6q28

The issue that bothers me the most is investing funds in organizations who are not contributing to making the world a better place. Creates a bit of a dilemma for me.